Ok so today's lesson covers the creation and implementation of a one-page financial dashboard for just about any business owner. These are the reports that you should have on hand.

I am going over this because almost all of us operate without understanding our actual financial position. We do not know what the exact reports are that we should be looking at and at what cadence. And I don't blame any of us. We are good at our specific trade/service. We are not accountants and speaking for myself, I really do not enjoy working with the numbers. So I really wanted to go over what we should be doing at a minimum.

Part 1: Foundation Requirements

Data Accuracy

Before we can build any dashboard, we need to make sure the numbers we're looking at are correct. So verify the below:

Your bank balance in QuickBooks matches what's actually in your bank account

Each expense is in the right category (meals aren't mixed with materials, gas isn't in office supplies)

You've entered all transactions from the past week

If you build a dashboard on bad data, you're making decisions based on fiction.

Essential Financial Statements

You need three core reports:

Balance Sheet

Shows what your business owns (trucks, equipment, cash) minus what you owe (loans, credit cards) equals what the business is actually worth. Think of it like your personal net worth but for your business.

Profit & Loss Statement

Shows all the money that came in this month minus all the money that went out. This tells you if you actually made money or just stayed busy.

Cash Flow Statement

Shows when money actually hit your bank account versus when you earned it on paper. You can show a profit on paper but have no cash to pay bills. This report explains why.

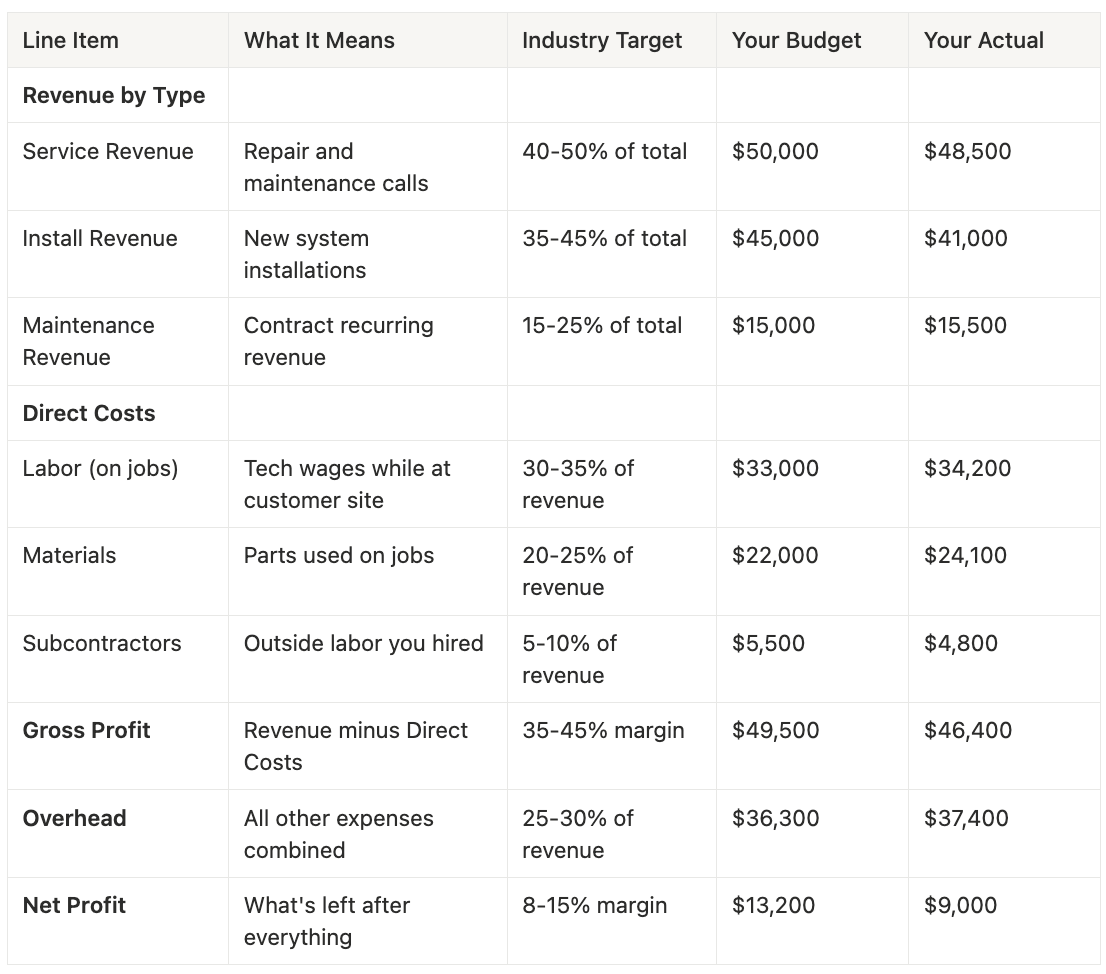

Part 2: Your One-Page Dashboard

The P&L Section

Your dashboard P&L tracks these key numbers against your budget:

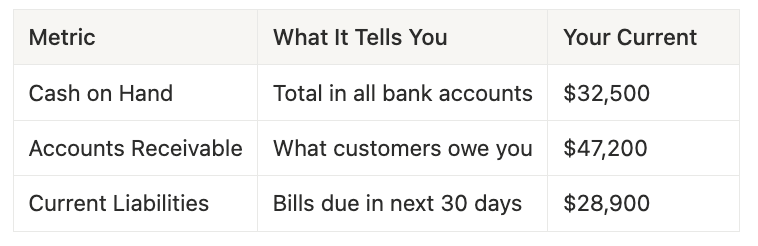

The Cash Section

Track these three numbers weekly:

Can your Cash + Receivables cover your Current Liabilities? If yes, you're ok. If no, start collecting money immediately.

Manual Entry Process

You need to manually enter these numbers every week. Not automated. Manual.

The act of typing in your revenue, your costs, your cash position forces you to actually look at them. You can't ignore a number you have to type.

Time requirement: 30 minutes weekly.

Part 3: Your Review Schedule

Daily (30 seconds)

Check your bank balance every morning. Open your banking app while you're having coffee. Look at the number. Know if you have $5,000 or $50,000 in there. This one habit prevents most cash emergencies.

Weekly (30 minutes)

Every Monday morning, update your dashboard:

Pull up your accounting software

Enter the month-to-date numbers into your dashboard

Compare actuals to budget

Identify anything that's off by more than 10%

Write down one action to fix the biggest problem

Monthly (60 minutes)

Close your books by the 10th of the following month. March ends on March 31st. By April 10th, all of March's receipts are entered, credit card transactions are recorded, and the month is "closed."

Then analyze:

Vertical Analysis: Look at everything as a percentage of sales. If materials were 20% last year and 25% this year, you know costs are creeping up.

Trend Analysis: Compare this month to your budget, last month, and the same month last year.

Quarterly (2-3 hours)

Review three-month trends and ask:

Do we need to adjust pricing?

Is overhead growing faster than revenue?

Are we saving enough for taxes?

Part 4: Pricing for Profit

Calculate Your Break-Even

Add up your annual costs:

Total overhead (rent, insurance, office staff): $200,000

Total direct labor cost (with taxes and benefits): $199,680

Total annual costs: $399,680

Calculate billable hours:

3 techs × 2,080 hours = 6,240 total hours

Minus vacation, training, drive time = 3,627 billable hours

Your break-even: $399,680 ÷ 3,627 hours = $110.21 per hour

This means charging less than $110.21 per hour guarantees you lose money.

Add Your Profit Margin

To get a true 20% profit margin: $110.21 ÷ 0.80 = $137.76 per hour

(Don't just add 20% to $110.21. That's markup, not margin, and you'll end up with less profit than you think.)

Use Flat Rate Pricing

Never quote hourly rates to customers. When you say "$150 per hour," they think about how long you're taking. When you say "Water heater replacement: $1,850," they think about the result.

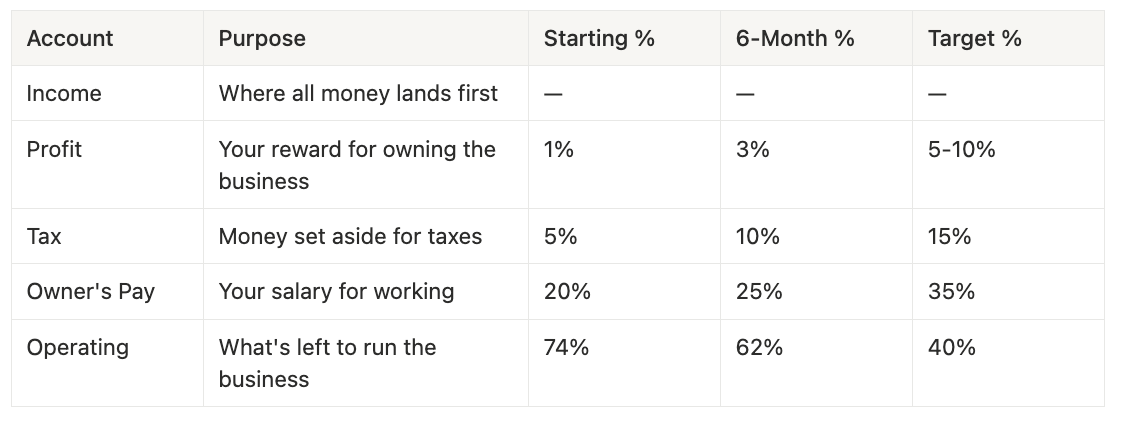

Part 5: Simple Cash Management

The Account System

Open separate bank accounts for different purposes:

Transfer Schedule

Twice a month on the 10th and 25th:

Look at what's in your Income account

Transfer the percentages to each other account

Pay bills only from Operating account

Start with just 1% to Profit. After three months, increase to 2%. Build the habit before you try to be aggressive.

Part 6: Your Team

Your accounting team has three roles. Sometimes it's three people, sometimes it's just you wearing three hats:

Bookkeeper: Enters receipts and transactions, categorizes expenses, sends you reports weekly

Accountant (CPA): Does your taxes, reviews everything quarterly, tells you how to legally pay less tax

You (Owner): Reviews the dashboard every Monday, makes decisions based on the data, owns the final responsibility

In a small company, you might do all three jobs. As you grow, hire people for the first two, but never delegate the third.

Bottom Line

This system will take some time to set up and require you weekly to maintain it. But I cannot recommend it enough.

You'll find where you're leaking cash. What services are consuming too much resource. Where you can adjust pricing. And so much more.

At the minimum just start with just the weekly dashboard.

You don't need to become an accountant. You just need to know enough about your numbers to make intelligent decisions. This system gives you exactly that.

As always, I hope this is thought provoking!

This is an incredibly practical, actionable guide for any operator. The emphasis on cash flow visibility, weekly financial discipline, and breaking even with clarity is what separates thriving businesses from the rest. It resonates strongly with the ground-level financial operational wisdom TCLM often shares - especially on managing working capital, trade terms, and liquidity for sustainable growth. If you're building out these financial systems, TCLM offers a useful free resource on the B2B finance side of things.

(It’s free)- https://tradecredit.substack.com/subscribe